Should you trust the stock market? Pt II

What if I told you there is a surefire way to invest in winners?

What if I told you about a method of stock selection that automatically dumps the losers—without requiring you to lift a finger?

And what if I then told you that this strategy costs less than other strategies, despite being more effective?!

You'd think I was a snake-oil salesman, right? But what if I'm telling you the truth, and the other guys are the snake oil salesmen?...

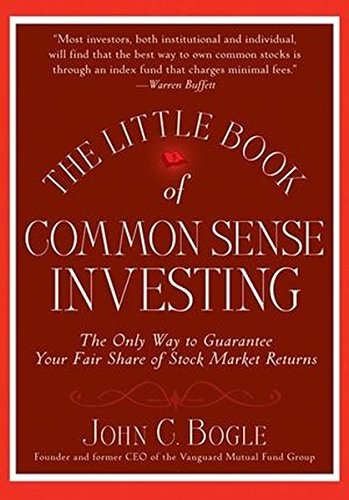

S&P 500 through 2015; graph from http://cbsnews1.cbsistatic.com/hub/i/2016/01/05/8bc2c493-ba40-4703-9979-c19534cbae20/64b19a4e258194bd5d72f1b77e371301/s-p-500-return-through-2015.gif

Jim Collins summarizes the argument well here: http://jlcollinsnh.com/2012/04/19/stocks-part-ii-the-market-always-goes-up/ The key point (okay, one of the key points) is this: "1. The market is self-cleansing...The market is not stagnant. Companies routinely fade away and are replaced with new blood."

He's also absolutely right that a company that's doing poorly will eventually fold and shares of its stock will be worth nothing and disappear. That's not so good, right? But what about the top companies? There's no limit to their growth!

This is what statisticians call a "floor effect." The simple summary is that there's a figurative 'floor' on how much money you can lose [all of it], but there's no 'ceiling' to limit how much money you can make [an unlimited amount!].

If you were to buy stock in every company, the 'losers' would eventually collapse and their stock would cease to exist. You would therefore lose money on the stock you bought in those companies. But the 'winners' will just keep growing, and giving you more and more return on your investment. The overall effect of this strategy is that you couldn't help but to make money!

Vanguard founder John Bogle's famous phrase to summarize this idea is: "Don't look for the needle in the haystack. Just buy the haystack."

Stock picking

Why bother buying the losers, then? Why not just buy the winners and get even more profit?

A lot of people get in trouble by trying to pick only the winners. Reams of research show that nobody can do it reliably. Nobody.

Not you, not your stockbroker, not the Wall Street hotshot who's taking a 1.5% cut of your investment dollars, not a well-designed computer program running a sophisticated algorithm buttressed with the latest developments in AI.

[As an aside, how could a computer program possibly pick better than a person? A person designs the computer program in the first place—a person who is probably more gifted at programming than at financial analysis! And, since there's no known set of indicators that reliably predict whether a stock is going to go up or down, how could the programmer know what to tell the program to look for?

In the absence of surefire predictor variables, the programmer feeds all the available data to the algorithm, and hopes the algorithm picks up on any patterns. But, of course, press releases—and fawning reporters—just focus on the promise of AI to inevitably conquer all of humanity's problems, including how to make money...]Jim Cramer of Mad Money fame is similarly unable to reliably pick winners. Does that give him even a moment's pause before hollering with complete self-assurance like a fool? Nope; humility would hurt his "brand!"

CNBC doesn't even bother to keep data about the performance of Cramer's picks...a ringing vote of confidence if I ever heard one! See p. 34 at this link for more detail about CNBC's record-keeping failures.

Now, I'm not trying to just pick on Jim Cramer or CNBC, because, as Daniel Solin writes here and I've written above, not a single person or organization can pick stocks that will beat the market, year after year, for a span of 20-30 years. Not one.

But that begs the question of why anyone should listen to Jim Cramer's advice in the first place!

If you were to give Cramer some sort of truth serum, he'd probably admit that his show is nothing more than entertainment for math/finance geeks, and people probably shouldn't act on his advice! After all, with famously wrong recommendations like this one, it's not like Cramer has a confidence-inspiring on-air track record.

Like any other mortal, Cramer is right sometimes, and he's wrong sometimes. And it turns out that in the long term, his picks end up performing about as well as if you just flipped a coin.

So why does Cramer have a long-running show while the proverbial coin flip doesn't? Well, Cramer's overconfident bluster is a great deal more entertaining than a coin flip! It's also more entertaining than level-headed analysis. And that's the only reason for his show's success.

How did Cramer get this show in the first place? He was a big-shot hedge-fund manager in the 1990s, which was a heyday for that type of investment. His self-reported success as a hedge fund manager (there's no independent audit to confirm that he was actually successful) and the success of his books led CNBC to give Cramer his own show.

In more recent years, hedge funds haven't done so well. There are certainly reasons for that, as the financial market in general exhibits different characteristics as it cycles through its phases. But retroactive descriptions of what factors made a particular type of investment perform well years ago are of little help today, as these factors are typically apparent only in retrospect.

That bears repeating: these factors are typically apparent only in retrospect. Those factors probably will not converge again during your lifetime...and even if they do, you probably won't realize it until it's already too late!

So it appears that hedge funds have had their day. It seems that a decline in the power, influence, and money available to hedge funds has begun.

The success—or lack thereof—of Cramer's publicly announced picks on Mad Money illustrates why.

However, nothing is certain in the financial world, and trends pull 180-degree turns on a regular basis. So who knows what the future holds?

The holy grail

The holy grail of the financial world is beating "the market" consistently. What is "the market?" An index, such as the Dow Jones or the S&P 500 (these are the most well-known, but not the only, such indices).

{kind=link}

{kind=link}

{kind=link}

I wrote above that a variety of studies have shown that fund managers can't beat the market for long stretches of time. Over a span of 3 years, sure, some actively-managed funds will beat their benchmark! But you're probably not investing for only 3 years; you're probably going to be in the market for many years, or even for decades.

If your investments beat the market for 3 years but underperform for 20, are you really better off? Check out the handy graphic to illustrate this effect at this USA Today article.

In one study, only 2 funds—out of nearly 3000!—remained in the top 25% of funds for 5 years running. Another study (reported here by CNBC, no less!) showed that passive investments nearly always outperformed actively-managed investments over a 10-year period. Here's a damning list of academic studies that all found similar results.

Behavioral finance research indicates that there's a good reason for this: our brains were shaped by evolutionary pressures that are very different from financial markets. Therefore, when it comes to investing, we tend to do the exact opposite of what we should do!

What's good for survival on the savanna isn't so good for your wallet on Wall Street.

Another explanation for this effect is the higher fees. Actively-managed funds require active managers, who want to get paid (and paid a lot) for their efforts. This necessitates higher fees than passively-managed counterparts that simply track an index.

Plus, there are fees for every time a company's stock is traded, which happens far more frequently in actively-managed funds than in passively-managed funds. The net result of all these fees? Less money in your pocket but more money in the pockets of financial professionals.

Conclusion? There's not a shred of good evidence that even full-time investment professionals can successfully and consistently pick winning stocks! And if you think you can—or if you think you'll pick a fund manager who can—you're deluding yourself.

What is an investor to do?

So, the holy grail of "beating the market" is unattainable over long periods of time. If you've ever heard the old adage "If you can't beat 'em, join 'em," you can probably guess what I'm about to say next.

You won't beat the market, so don't even try!

Fortunately, it's a pretty simple matter to nearly match the market: passively-managed index funds. Pick an index, and you can find a low-fee fund that matches it. There's still going to be a management fee, but that's basically unavoidable.

The good news is that this fee will be minimal compared to actively-managed funds; look for an "expense ratio" (as such fees are typically named) around 0.20% or less. This is much less of a drag on your returns than the fee of over 1.00% that most actively-managed funds charge, and this savings compounds over time.

There are great descriptions of the advantages of passively-managed funds (like index funds) here and here. On the first page of this book chapter, John Bogle, the founder of Vanguard, lays out a compelling argument for index investing.

The case against indexing

And what of Dan Wiener's objection to index-fund investing as laid out in the subsequent quote on pages 1-2 of that book chapter? The authors found mixed support, writing that Wiener's assertion is "suspect" (p. 26), though Wiener objects to the test employed therein.

Charlatans never allow their claims to be tested, because a test raises the possibility of being proven wrong. Is Wiener a charlatan? I don't think so, despite his noted disdain for index investing. According to this article, Wiener's investment firm, Adviser Investments, outperforms the S&P 500 by 2% over the long term. How long is that "long-term" record? The article doesn't specify; 10 years is often considered "long-term" in the financial world, so that's a reasonable guess, but it's just that: a guess.

Such a record does, indeed, suggest that Wiener's approach may be better than just plopping your money in an index fund and forgetting about it. However, it's impossible to know if that '2% outperformance' figure really includes such factors as taxes, transaction fees, management fees, dividend reinvestment, etc. It's certainly possible to beat an index fund through smart diversification of your investments, particularly by investing in mutual funds that specialize in small-cap value stocks, but the question is whether the extra fees are worthwhile. (See the graph from Vanguard, below)

Wiener's broad condemnation of index-fund investing as a "lousy investment" that "works for Vanguard]" rather than for the individual investor betrays, at best, a lack of long-term vision. He says that "the big famous Index funds at Vanguard have chronically underperformed over the last few years."

Underperfomed compared to what? And how many years is "the last few?" Wiener, writing in 2007, doesn't specify. And that lack of specificity makes me wary. Also note that the quote is from before the big market crash of 2008. So, if Vanguard's index funds underperformed active investing strategies between the tech bubble in 2001 and the housing crash in 2008 but outperformed them afterward, that tells me that Wiener's active investing strategy does well during boom times but is dangerous during busts.

Such a pattern could very easily give the long-term performance edge to index funds (not to mention that indexing liberates you to spend your time thinking about things other than the stock market).

There will always be times at which index investing underperforms active investments, such as the bull market of the 1990s that yielded good times for hedge funds. The point is that, when those market conditions change, a "chronic underperformer" like an index fund between 2003 and 2007 (which is likely the period to which Wiener is referring) could suddenly outperform those same active investments by a factor of 10! And there's no telling when such a shift in market conditions will occur, hence, the importance of diversification.

The point of passive index investing isn't that it will outperform active investments for a period of a few years. Index investors are in it for the long haul—measured in decades—with changing market conditions, changing legal conditions, and a changing landscape of opportunities. There is no single strategy that will outperform the index through all of these changes, and trying to pick someone who will successfully guide you through them all is a fool's errand!

Despite a mountain of evidence to the contrary, as described above, Wiener claims that you can, in fact, pick good managers. Perhaps he can. He's the CEO of an investment firm and editor of an investment newsletter. I'm neither, and if you're reading this, I bet you're in the same boat as I am.

If I pick a fund manager who happens to repeatedly beat the S&P 500, I can assure you that it was blind luck! And even if I luck into picking a great manager, the probability that this great manager will continue to outperform the S&P 500 by the time I'm 68 (i.e. 40 years from now) is virtually zero.

So I either have to trust Mr. Wiener and buy his newsletter every year and/or pay annual fees for the advice of people who work for his firm...or else plop my money in an index fund and trust that this trend will continue.

I have a lot more faith in this...

{kind=link}

...than in some random person's ability to have his or her finger "constantly on the pulse of the ever-changing market" and to make the right calls based on that "pulse:"

The best-case scenario is that Mr. Wiener's statement betrays a myopic focus on the short-term: "see, my picks beat this index between Year X and Year Y. Therefore, index funds are terrible investments!" This would illustrate confirmation bias at its finest. Wiener certainly wouldn't be alone in exhibiting such a short-term focus!

But at worst, one could easily accuse Mr. Wiener of giving self-interested advice. After all, if you subscribe to the passive-investing philosophy, what reason would you have to pay Wiener for his newsletter? Or for the services of his investment firm? So he has every reason to paint index investing in a negative light.

Maybe he can beat the S&P 500 over the next 40 years. But I wouldn't hold my breath. After reading the bit quoted in that book chapter, I wouldn't give him $350,000, either!

To be fair to Wiener, I'll note that his statement about index investing being in Vanguard's interest isn't entirely wrong. Vanguard's business is largely predicated upon its clients' faith in low-cost index investing. Vanguard does do rather well for itself by convincing people to buy its services.

But this argument that the strategy either works in favor of Vanguard or in favor of the client assumes that investing is a zero-sum endgame. But it's entirely possible—in fact, I'd argue that it's downright desirable—for both parties to make money in a fair exchange!

- Vanguard sets up whatever systems are necessary and hires whatever people are necessary to make the index fund work. Without them, you'd have to check on your preferred index and see if that index has changed any of its holdings. Then it would no longer be a passive investment strategy, as it would require plenty of time and attention from you!

Isn't that in the long-term best interest of everyone?

The case for indexing

In that statement, Weiner asserts that "faith in indexing" is "a lie."

I'll post the S&P 500 historical graph yet again. You tell me: is this a lie?

Looks pretty honest to me! But if you don't believe it, I encourage you to check the S&P 500's historical performance for yourself. You can make your own decisions; I have nothing to hide, and nothing to gain from misleading you or distorting the picture of what's going on.

Remember the discussion of the 'floor effect' at the beginning of this piece? Remember how the losers go away but the winners keep making money? And new companies replace the losers? That's what drives the effect shown above.

That is the literal opposite of a "lie." It is a simple, indefinitely sustainable, and extremely powerful engine that drives returns over the long term.

In short? You're looking at the heart of capitalism.

Index investing is betting on capitalism itself. And, given that the term 'capitalism' dates back to the 1600s (but the basic principles are as old as civilization itself), there's no question that capitalism fundamentally works. A bet that capitalism will persist in the future is about the only bet I'm actually willing to take!

Debate remains regarding the particulars. For example: should you use an American-only index, or should you add international indices as well? The answer ultimately comes down to how much faith you have in the long-term health of the United States economy.

Further corroboration for my point: Leland Faust, founder of CSI Capital Management, recommends investing in a handful of index funds (including bond funds). As the German researcher and author Gerd Gigerenzer aptly put it when describing how to make a prediction: "...if you are in an uncertain world, make it simple. If you are in a world that's highly predictable, make it complex."

Hopefully, you're convinced by now that your best bet is to sink your money into an index fund and then go about your life and ignore the ups and downs of the stock market. But if you're not convinced yet, I'll give it one last shot.

A case study: The Dow Jones

Consider the Dow Jones Industrial Average. It consists of stock in 30 of the top publicly traded companies headquartered in the United States. The Dow is a scaled average that's weighted to compensate for a number of factors. A solid summary of the Dow Jones can be found here.

Who determines what warrants inclusion in this index? Good question! The companies listed on the Dow Jones are ultimately picked by a panel of people. When considering a company for inclusion on the Dow, the panel doesn't just consider a company's profitability, but also the longevity of that profitability.

As with any human endeavor, the members of the panel may be biased and/or behind the times. Their selections are not necessarily beyond reproach. But that's beyond the point I want to make here.

The point I want to emphasize is: what happens when a company stops doing well? I'm not talking about doing poorly for a day, a week, or even a month. But what happens when a company stops doing well for an extended period of time, or the company's primary market changes rapidly and that company isn't well-positioned to take advantage of the new trend?

The answer is that the company is removed from the index and replaced with one that is in better financial health.

Jim Collins' point about the market being "self-cleansing" is thereby realized from an index investor's point of view. A given index like the Dow Jones or the S&P 500 is, to some degree, self-cleansing. But it's also resistant to overreaction based on a bad day, a bad week, or a bad month. As far as I'm concerned, that's a pretty ideal scenario, especially for a young investor!

Just sink a significant proportion of your investments into a passively-managed stock market index fund, and then go about your life. These are some S&P 500-based options; be aware that there are numerous other alternatives (not all of which are based on the S&P 500).

Where the rubber meets the road

How much should you put into your index fund investment?

Ah, that's the million-dollar question! Everybody has an opinion; some are wildly different!

For example: Jim Collins makes the case that you can often go with 100% of your allocation in VTSAX, the Vanguard Total Stock Market Index Fund. I think this is reasonable and defensible, and he lays out a good case for it again here. If you buy his argument (and mine!) that the market always goes up in the long-term, then you can buy into the entire market with VTSAX. I believe that's a good bet.

But at the other end of the spectrum, Paul Merriman—who I also like and respect—recommends a much more nuanced inclusion of various Vanguard products. See an article here that encourages readers to avoid relying on an S&P 500 fund (and Merriman isn't the only one saying that, either).

For a more detailed analysis, check out Merriman's free e-book here. I'll direct you to page 90 (page 107 of the PDF, including the cover and preliminary pages) for his model portfolio suggestions in a handy table format. Merriman's recommendations include an S&P 500 index fund, a small-cap index fund, a REIT index, an international value index, and more.

You can find a dizzying array of different Vanguard funds, along with their expense ratios and average returns over various timeframes, at this link. How do you pick from among so many different options? Well, it depends on your own personal preferences, risk tolerance, and situation.

If you're just beginning your career, the best portfolio for your needs will look very different than if you're 5 years away from retirement. That's why a fiduciary financial advisor is the best—and if you want advice that's in YOUR best interest, the only—choice to help you iron out your asset allocation.

A personal example

I give you an example that works for my situation, and possibly not for anyone else's. I'm in my 20s, single, and a grad student who makes precious little money. I have a little bit of money as a cushion against disaster; an "emergency fund," if you will. I have a decent tolerance for risk, as I have plenty of time to let the market make up for any dips in performance.

Example 1: For myself, I like the following allocation from Vanguard's selections: 50% of my portfolio in VTSAX, Vanguard's Total Stock Market Index Fund. Another 10% in a value fund like VVIAX or VTV provides extra growth potential. Another 10% in an emerging markets fund like VEMAX, or an international value fund like VTRIX, or an international growth fund like VWIGX would bring me to 70%. Putting an additional 15% in a REIT index fund like VGSLX (or VNQ, an equivalent ETF) and 15% in a bond index fund like VBTLX or VLTCX would round out this portfolio.

- Some might think the inclusion of 10% in either VEMAX, VTRIX, or VWIGX, along with 15% in a REIT fund like VNQ, makes me a riverboat gambler. I'd disagree; I think that gives me a nice exposure to asset classes that tend to do well at different times than a fund like VTSAX.

One of these funds might lose money, but it's unlikely that all of them will lose money at the same time! And the 15% in bonds gives me a dose of stable appreciation. To me, this represents a solid mix of asset classes that's pretty straightforward and simple to understand.

Someone else might replace VEMAX/VTRIX/VWIGX with a fund in the health care sector, such as VGHCX, or a fund in the energy sector, such as VGENX, as these have performed pretty well historically, though they're more volatile than the total market fund would be.

- Here's the bottom line for Example 1:

- 50% of my money in VTSAX ($10,000 minimum investment; an ultra-low expense ratio of 0.05%)

- 10% in VTV (no minimum; expense ratio of 0.08%)

- 10% in VWIGX ($3,000 minimum; expense ratio of 0.46%)

- 15% in VNQ (no minimum; expense ratio of 0.12%)

- 15% in VBTLX ($10,000 minimum; expense ratio of 0.06%)

- Compare these expense ratios—all of which are less than 0.50%—to those of competitors like those listed here or here.

- What's the big deal about this? 1% still isn't that much, right?! Check out this graph prepared by Vanguard, and you tell me: is almost $94,000 chump change to you?!

- So yeah, a 0.9% difference is a HUGE deal! [Not to mention that some investment products are even more expensive than that...]. Oftentimes, you'll be much better off by choosing the lowest-cost investment.

- This simple allocation would give someone a healthy dose of bonds via VBTLX. Since bonds tend to be stable and exhibit little volatility, this is a good choice for a conservative investor. VTSAX provides a position in stocks of all the publicly traded companies in the U.S., and VTWSX provides stocks from the U.S. and around the world.

- Here's what this looks like:

- 50% in VBTLX ($10,000 minimum; 0.06% expense ratio)

- 25% in VTSAX ($10k minimum; 0.05% ER)

- 25% in VT (no minimum; 0.11% ER)

Even though the entire history of civilization points to the fact that capitalism works and your money is safe in stocks in the long term, it's entirely understandable if you want to hedge your bets and reduce volatility by putting some money into bonds.

_________________________

Finally, for evidence that Jim Collins and I aren't alone in expecting the stock market to increase in value over time: https://www.financialfixation.com/single-post/2017/01/25/Dow-20K---Whats-the-Big-Deal-Anyways and http://www.ivigilante.com/taming-the-hulk/.

If you're looking for a more buttoned-down and academic version of this argument, you may prefer Vanguard's article here or here, the latter of which refers back to this 1986 paper.

_________________________

That wouldn't surprise me, and if it happens, it shouldn't surprise you, either! And that illustrates why index investing can be so powerful...

If you want to know more, a great place to start is John Bogle's

No comments:

Post a Comment